Category: Meanderings

Playing Through

Tom Peters shares how starting something dull … check out his stories of Jim and Larry. Are you ready to be boring?

via youtube.com

Not sure what you want to do when you grow up? Tom Peters suggests starting something dull or boring and sticking with it. The wisdom of the “millionaire next door” is this:

• They lived in the same town their entire life.

• They’re the first generation that’s wealthy; had no parental support at all.

• Don’t look like millionaires, don’t dress like millionaires, don’t eat like

millionaires, don’t act like millionaires.

• And most of their businesses, to quote the author, are businesses that could be called “dull.”

And so you want to know what you ought to do when you grow up? Why don’t you get into the dog walking business? Why don’t you clean mold out of basements? Which is to say, anything—in fact, even the stuff that sounds the most dull—can be seriously cool, seriously fun, and seriously profitable.

Seth Godin asks great questions: Does your job happen to you (victim) OR are you creating the change?

Does your job happen to you?

If you’re a willing cog in the vast machinery of work, it’s entirely possible that the things that occur all day feel like they’re being done to you.

The alternative is to create a job where you create forward motion, where you do things to the job, not the other way around.

Take a look at the language you use to describe what happened at work yesterday, that’s your first clue. If you’re not the one creating the change, perhaps it’s time to start.

Seth always pushes my buttons … gotta make some change today (and not just for my kids’ lunch money)!

Roger Lowenstein says do what Wall Street does … Walk Away From Your Mortgage! via The New York Times

John Courson, president and C.E.O. of the Mortgage Bankers Association, recently told The Wall Street Journal that homeowners who default on their mortgages should think about the “message” they will send to “their family and their kids and their friends.” Courson was implying that homeowners — record numbers of whom continue to default — have a responsibility to make good. He wasn’t referring to the people who have no choice, who can’t afford their payments. He was speaking about the rising number of folks who are voluntarily choosing not to pay.

Such voluntary defaults are a new phenomenon. Time was, Americans would do anything to pay their mortgage — forgo a new car or a vacation, even put a younger family member to work. But the housing collapse left 10.7 million families owing more than their homes are worth. So some of them are making a calculated decision to hang onto their money and let their homes go. Is this irresponsible?

Businesses — in particular Wall Street banks — make such calculations routinely. Morgan Stanley recently decided to stop making payments on five San Francisco office buildings. A Morgan Stanley fund purchased the buildings at the height of the boom, and their value has plunged. Nobody has said Morgan Stanley is immoral — perhaps because no one assumed it was moral to begin with. But the average American, as if sprung from some Franklinesque mythology, is supposed to honor his debts, or so says the mortgage industry as well as government officials. Former Treasury Secretary Henry M. Paulson Jr. declared that “any homeowner who can afford his mortgage payment but chooses to walk away from an underwater property is simply a speculator — and one who is not honoring his obligation.” (Paulson presumably was not so censorious of speculation during his 32-year career at Goldman Sachs.)

The moral suasion has continued under President Obama, who has urged that homeowners follow the “responsible” course. Indeed, HUD-approved housing counselors are supposed to counsel people against foreclosure. In many cases, this means counseling people to throw away money. Brent White, a University of Arizona law professor, notes that a family who bought a three-bedroom home in Salinas, Calif., at the market top in 2006, with no down payment (then a common-enough occurrence), could theoretically have to wait 60 years to recover their equity. On the other hand, if they walked, they could rent a similar house for a pittance of their monthly mortgage.

There are two reasons why so-called strategic defaults have been considered antisocial and perhaps amoral. One is that foreclosures depress the neighborhood and drive down prices. But in a market society, since when are people responsible for the economic effects of their actions? Every oil speculator helps to drive up gasoline prices. Every hedge fund that speculated against a bank by purchasing credit-default swaps on its bonds signaled skepticism about the bank’s creditworthiness and helped to make it more costly for the bank to borrow, and thus to issue loans. We are all economic pinballs, insensibly colliding for better or worse.

The other reason is that default (supposedly) debases the character of the borrower. Once, perhaps, when bankers held onto mortgages for 30 years, they occupied a moral high ground. These days, lenders typically unload mortgages within days (or minutes). And not just in mortgage finance, but in virtually every realm of our transaction-obsessed society, the message is that enduring relationships count for less than the value put on assets for sale.

Think of private-equity firms that close a factory — essentially deciding that the company is worth more dead than alive. Or the New York Yankees and their World Series M.V.P. Hideki Matsui, who parted company as soon as the cheering stopped. Or money-losing hedge-fund managers: rather than try to earn back their investors’ lost capital, they start new funds so they can rake in fresh incentives. Sam Zell, a billionaire, let the Tribune Company, which he had previously acquired, file for bankruptcy. Indeed, the owners of any company that defaults on bonds and chooses to let the company fail rather than invest more capital in it are practicing “strategic default.” Banks signal their complicity with this ethos when they send new credit cards to people who failed to stay current on old ones.

Mortgage holders do sign a promissory note, which is a promise to pay. But the contract explicitly details the penalty for nonpayment — surrender of the property. The borrower isn’t escaping the consequences; he is suffering them.

In some states, lenders also have recourse to the borrowers’ unmortgaged assets, like their car and savings accounts. A study by the Federal Reserve Bank of Richmond found that defaults are lower in such states, apparently because lenders threaten the borrowers with judgments against their assets. But actual lawsuits are rare.

And given that nearly a quarter of mortgages are underwater, and that 10 percent of mortgages are delinquent, White, of the University of Arizona, is surprised that more people haven’t walked. He thinks the desire to avoid shame is a factor, as are overblown fears of harm to credit ratings. Probably, homeowners also labor under a delusion that their homes will quickly return to value. White has argued that the government should stop perpetuating default “scare stories” and, indeed, should encourage borrowers to default when it’s in their economic interest. This would correct a prevailing imbalance: homeowners operate under a “powerful moral constraint” while lenders are busily trying to maximize profits. More important, it might get the system unstuck. If lenders feared an avalanche of strategic defaults, they would have an incentive to renegotiate loan terms. In theory, this could produce a wave of loan modifications — the very goal the Treasury has been pursuing to end the crisis.

No one says defaulting on a contract is pretty or that, in a perfectly functioning society, defaults would be the rule. But to put the onus for restraint on ordinary homeowners seems rather strange. If the Mortgage Bankers Association is against defaults, its members, presumably the experts in such matters, might take better care not to lend people more than their homes are worth.

Roger Lowenstein, an outside director of the Sequoia Fund, is a contributing writer for the magazine. His book “The End of Wall Street” is coming out in April.

Sign in to Recommend More Articles in Magazine » A version of this article appeared in print on January 10, 2010, on page MM15 of the New York edition.

via nytimes.com

I am glad that I am able to make the mortgage payment on our home, and I intend to keep making it! On the other hand, recent news from Wall Street suggests that the moral argument to “send the right message” by being faithful in your payments has no real basis in the business world. For that we will have to run theology and ethics … both of which may be in short supply on the street.

Howard Thurman reminds us that Christ belongs in every season via God’s Politics Blog

When the song of the angels is stilled,

when the star in the sky is gone,

when the kings and princes are home,

when the shepherds are back with their flock,

the work of Christmas begins:

to find the lost,

to heal the broken,

to feed the hungry,

to release the prisoner,

to rebuild the nations,

to bring peace …

to make music in the heart.

– Howard Thurman

American author, civil rights leader, and theologian (1899-1981)

via Voice of the Day: Howard Thurman – God’s Politics Editor – God’s Politics Blog.

Voice of the Day: Howard Thurman via God’s Politics Blog

When the song of the angels is stilled,

when the star in the sky is gone,

when the kings and princes are home,

when the shepherds are back with their flock,

The work of Christmas begins:

to find the lost,

to heal the broken,

to feed the hungry,

to release the prisoner,

to rebuild the nations,

to bring peace …

to make music in the heart.

– Howard Thurman

American author, civil rights leader, and theologian (1899-1981)

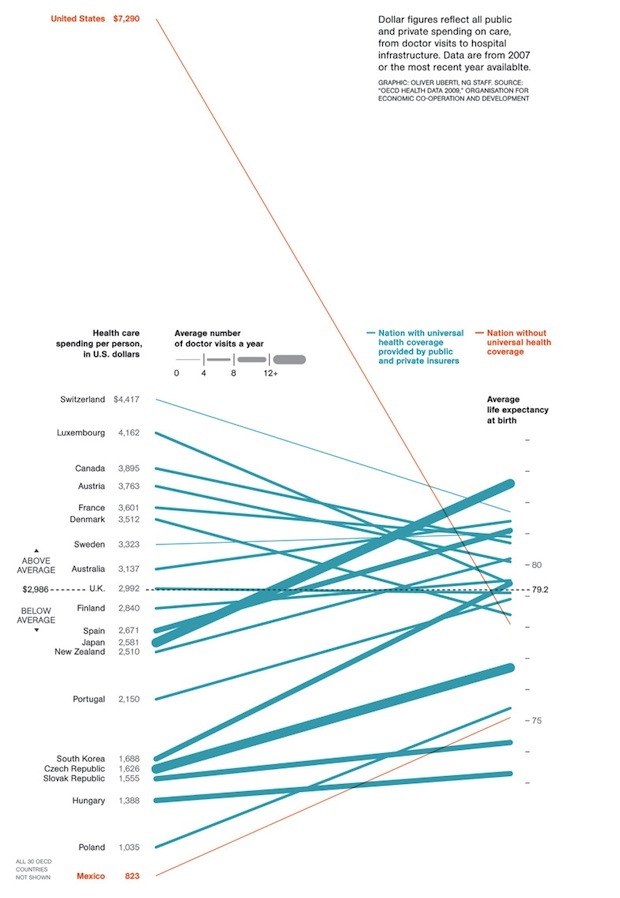

OUCH! How Bad Is U.S. Health Care? Infographic of the Day via Fast Company

Is College Really Worth It? The answer is a mixed bag. via Fast Company’s Infographic of the Day

Shane Claiborne – Letter to Non-Believers by Shane Claibourne – Esquire

I want to invite you to consider that maybe the televangelists and street preachers are wrong — and that God really is love. Maybe the fruits of the Spirit really are beautiful things like peace, patience, kindness, joy, love, goodness, and not the ugly things that have come to characterize religion, or politics, for that matter. (If there is anything I have learned from liberals and conservatives, it’s that you can have great answers and still be mean… and that just as important as being right is being nice.)

The Bible that I read says that God did not send Jesus to condemn the world but to save it… it was because “God so loved the world.” That is the God I know, and I long for others to know. I did not choose to devote my life to Jesus because I was scared to death of hell or because I wanted crowns in heaven… but because he is good. For those of you who are on a sincere spiritual journey, I hope that you do not reject Christ because of Christians. We have always been a messed-up bunch, and somehow God has survived the embarrassing things we do in His name. At the core of our “Gospel” is the message that Jesus came “not [for] the healthy… but the sick.” And if you choose Jesus, may it not be simply because of a fear of hell or hope for mansions in heaven.

You must be logged in to post a comment.